Contents

- 📈 What Exactly is the Compound Interest Formula?

- 💡 Who Needs to Understand This Formula?

- 🧮 The Core Components: Breaking Down the Math

- 🚀 How Compound Interest Accelerates Growth

- 🤔 Common Misconceptions & Pitfalls

- ⚖️ Compound Interest vs. Simple Interest: A Crucial Distinction

- 🛠️ Tools & Calculators for Practical Application

- 📚 Further Learning & Resources

- Frequently Asked Questions

- Related Topics

Overview

The compound interest formula is the bedrock of wealth accumulation, describing how an investment's earnings—principal plus accumulated interest—begin to earn their own interest. It's not just a mathematical curiosity; it's the engine that powers long-term financial growth. At its heart, the formula quantifies the snowball effect, where your money works harder for you over time. Understanding this formula is crucial for anyone serious about building wealth, whether through savings accounts, investments, or understanding debt.

💡 Who Needs to Understand This Formula?

Anyone with financial goals should grasp the power of the compound interest formula. This includes individuals saving for retirement, planning for a down payment, or even managing debt. Small business owners can use it to project loan growth or investment returns. Financial advisors rely on it daily to model client portfolios. Even students learning basic personal finance principles will encounter its fundamental importance in understanding how money grows.

🧮 The Core Components: Breaking Down the Math

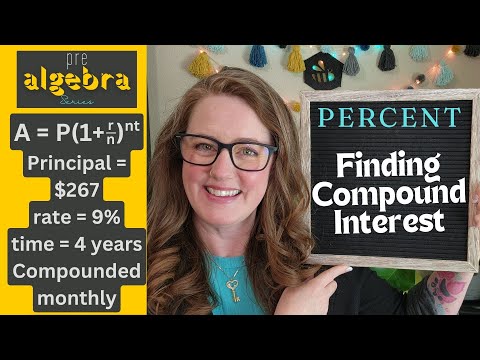

The fundamental compound interest formula is typically expressed as A = P(1 + r/n)^(nt). Here, 'A' represents the future value of the investment/loan, including interest. 'P' is the principal amount—the initial sum of money. 'r' is the annual interest rate (expressed as a decimal). 'n' is the number of times that interest is compounded per year. 't' is the number of years the money is invested or borrowed for. Each variable plays a critical role in determining the final outcome.

🚀 How Compound Interest Accelerates Growth

The magic of the compound interest formula lies in its exponential nature. Unlike simple interest, which only calculates interest on the initial principal, compound interest calculates interest on the principal and the accumulated interest. This means your earnings start generating their own earnings, leading to significantly faster growth over extended periods. A small difference in the interest rate or compounding frequency can lead to vast differences in the final amount after decades.

🤔 Common Misconceptions & Pitfalls

A common misconception is that compound interest only applies to savings accounts. In reality, it also works against you with credit card debt or loans. Another pitfall is underestimating the impact of time; people often start too late, missing out on the most powerful phase of compounding. Many also overlook the effect of compounding frequency ('n'), assuming annual compounding is the only type, when more frequent compounding (monthly, daily) yields greater returns.

⚖️ Compound Interest vs. Simple Interest: A Crucial Distinction

The distinction between compound interest and simple interest is stark and critical. Simple interest is calculated only on the initial principal amount. For example, $100 at 5% simple interest for 10 years yields $50 in total interest ($5 per year). The same $100 at 5% compound interest, compounded annually, for 10 years yields approximately $62.89 in total interest. The difference might seem small initially but becomes enormous over longer durations.

🛠️ Tools & Calculators for Practical Application

While understanding the compound interest formula is key, practical application is often best achieved with tools. Numerous online calculators are available that allow you to input your principal, interest rate, compounding frequency, and time period to instantly see the projected future value. Many brokerage platforms and banking apps also offer built-in calculators. Spreadsheets like Microsoft Excel or Google Sheets can also be used to model compound growth with formulas.

📚 Further Learning & Resources

For a deeper understanding of the compound interest formula and its implications, explore resources on financial mathematics and investment strategies. Books like 'The Intelligent Investor' by Benjamin Graham, while not solely focused on the formula, illustrate its power through long-term investing principles. Reputable financial education websites and courses often dedicate modules to explaining compounding's mechanics and strategic use.

Key Facts

- Category

- topic

- Type

- topic

Frequently Asked Questions

What is the most important factor in compound interest?

Time is arguably the most critical factor. The longer your money is invested and compounding, the more significant the growth becomes due to the snowball effect. While interest rate and compounding frequency are vital, starting early maximizes the impact of time, allowing even modest sums to grow substantially.

How often should interest be compounded for maximum benefit?

For the investor, more frequent compounding is generally better. Compounding monthly or daily results in slightly higher returns than compounding annually because the interest earned starts earning interest sooner. However, the difference between daily and monthly compounding is often marginal compared to the impact of the interest rate and time.

Can compound interest be used for debt repayment?

Absolutely, but it works against you. High-interest debts like credit cards often use compound interest, meaning the interest accrues on the principal and previously unpaid interest. Understanding this formula highlights the urgency of paying down such debts quickly to avoid substantial long-term costs.

What's the difference between the formula and a calculator?

The formula is the mathematical equation that defines how compound interest works. A calculator is a tool that uses this formula to perform the calculations for you quickly and easily. While understanding the formula provides insight, calculators are practical for everyday financial planning and projections.

Does the principal amount matter significantly?

Yes, the principal amount is the starting point for your growth. A larger principal will naturally result in larger absolute interest earnings, even at the same interest rate and compounding period. However, the power of compounding means that even small initial principals can grow substantially over long periods.

Are there any taxes to consider with compound interest?

Yes, depending on the type of account and jurisdiction, earnings from compound interest may be subject to taxes. For example, interest earned in a regular savings account is typically taxed annually. Tax-advantaged accounts like IRAs or 401(k)s allow interest to compound tax-deferred or tax-free, significantly enhancing long-term growth.